Craving Commodities

Why we love investing in commodities

“In a commodity business, it’s very hard to be smarter than your dumbest competitor.” — Warren Buffett

“Beware when investing in commodities, where price is king—especially when other governments are subsidizing them.” — John Doerr, Speed & Scale

Those investors might not like commodities, but we do.

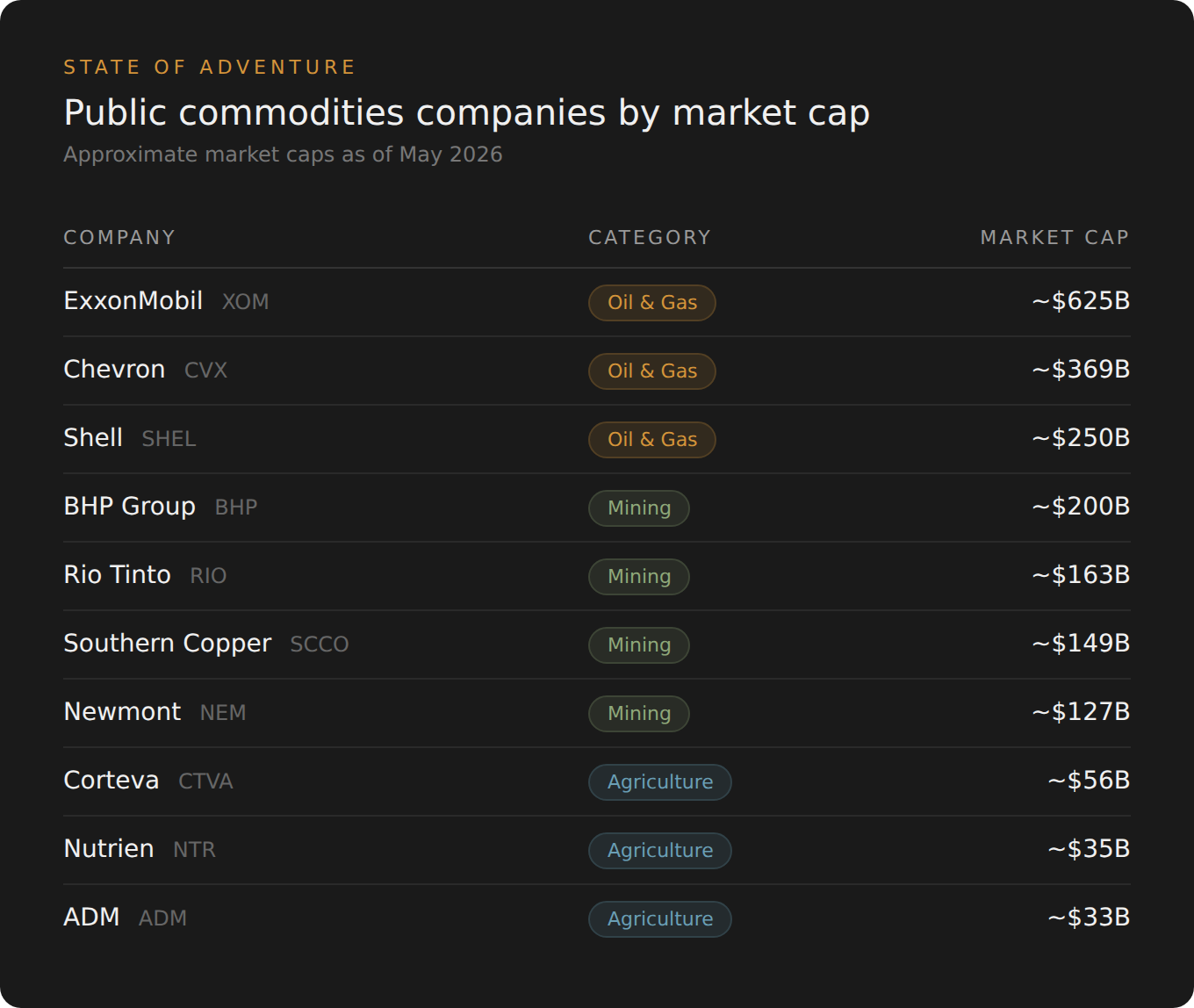

Most investors shy away from commodities because they imply heightened competition and structurally lower margins (and returns). But there are benefits — commodities imply massive scale, and many of the incumbents are huge as a result.

Now, not all these companies have represented attractive investment opportunities the last few decades; the takeaway is rather that their size warrants evaluation.

The magnitude of the size matters. We joke that one of the ways Cantos evaluates opportunities is by looking at the top public companies by market cap (and founding year) and going down the list to find outdated and antiquated ones that could be reimagined.

“Let me tell you something. Size does matter. Don’t let anyone tell you different.” — Justin Hammer

We’re betting on the idea that new commodity companies will in fact be attractive investments. Massive ones. Precisely because they use technology to arrive at a fundamentally superior cost profile.

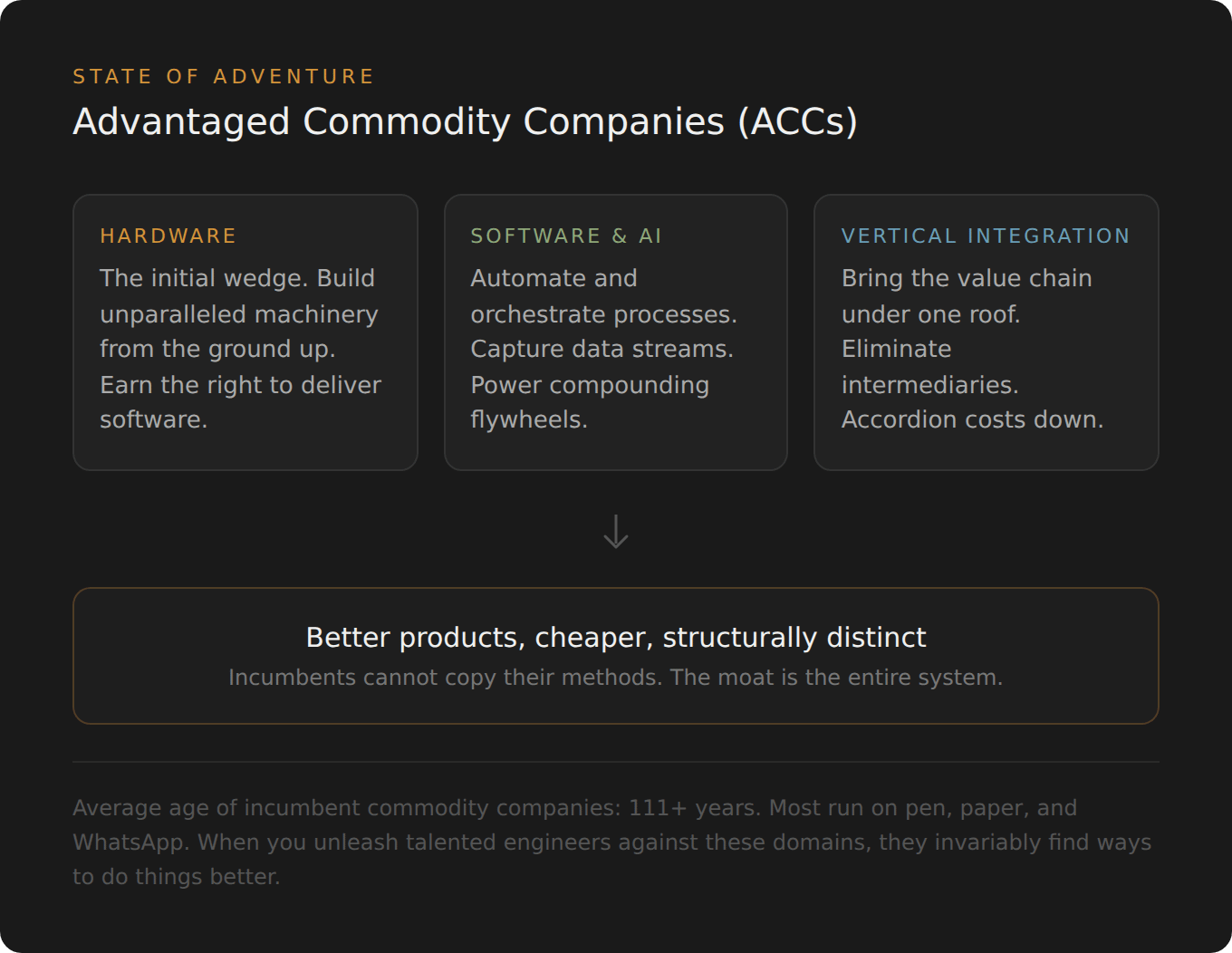

We call these Advantaged Commodity Companies (ACCs), and they’re one of the investment areas we’re most excited about.

Advantaged Commodity Companies do 3 things: They use hardware to make products and processes better, faster, and cheaper; they use software & AI to automate and orchestrate their processes; and they use vertical integration to accordion costs down.

The end result is a company that produces better products, for cheaper, and does so in a way that’s counter positioned to the incumbents. It’s structurally distinct enough that incumbents cannot copy their methods.

The reason why we like ACCs so much is that they have incredible durability. They require immense work, and it takes serious investment to hit scale, but if you get there, you are alone. Competitively, yes, there are big incumbents. But the average age of these companies is over 111 years old. The only software they might have is WhatsApp, Gmail, and maybe Microsoft Office. Most operate on pen and paper. Some are more forward looking than others, but the technological pace of development grossly lags behind.

When you unleash talented engineers against these domains they invariably find ways to do things better. That’s why hardware is often one of the best initial wedges. If you take aerospace and defense engineers and let them create critical machinery from the ground up, they usually end up with unparalleled hardware. In some cases, this hardware does something never possible before. Shinkei’s Poseidon robot is a canonical example. No one else has found a way to automate the Japanese Ike-jime technique.

As we say, Hardware is the Trojan Horse for Software. Once you have your hardware, you can introduce software to the equation. But you have to get there to earn the right to deliver it. In some cases you might already know what you’ll introduce. In some cases, like AWS and Starlink, you stumble upon the big solution later on.

Once you have hardware and software in place, ACCs are able to acquire unparalleled data streams. All of our portcos have higher data fidelity than their competitive peer set, largely thanks to computer vision, custom software, and even simple digitization practices. The addition of data capture + observability lead to powerful data flywheels.

Processes are the least sexy but most invaluable part of the equation: Every single ACC we’ve backed has heard this phrase repeatedly: “We’ve never thought of that before.” When you bring fresh perspectives to an industry reliant upon the status quo and you ask a lot of questions, you invariably uncover golden opportunities to do things differently. These end up becoming the deepest moats. Especially because tacit knowledge in these industries is not online. LLMs don’t know about it, which means new entrants have harder times finding it. You have to actually go out into the world to learn, and even that pales in comparison to doing the thing yourself.

Lastly, there’s vertically integration. We’ve written a lot about this already, but the key aspect here is that most often, the number of intermediaries means that if you bring additional parts of the value chain under your roof, there’s meaningful performance and cost gains. It needs to be wielded surgically, not haphazardly.

Finally, we want founders that are Maze Historians. They should be encyclopedic about the given category they’re operating in. The reason is that usually there have been plenty of prior attempts at building new companies in these respective categories. And if you don’t know why they succeeded (or more likely failed), you’ll be less likely to survive and thrive. The structure of an industry provides clues, and we want the founding team to be proper detectives to dissect the what and why. That is how you can arrive at business model insights that further drive counter positioning.

All of these factors must contribute to cost. If the market price for a good is already on the floor, there’s not much room to improve that process. One of the failure modes of some Cleantech investments is they hoped for a willingness to pay that was above the market clearing price for the good they were competing against. We don’t want that. We want companies that outright win on price.

If you combine all of these dynamics together, you’ll put yourself in a position to build a massively scaled business. None of this is easy, but we believe the reward is more than worth it.

What does this look like? Amazon.com

Now I know what you’re thinking, but bear with me. The original Amazon store only offered books. Yes, every book is different, but different copies of books are the same. The thing that mattered was offering a large enough selection at attractive prices and being able to deliver orders to customers. Bezos was adamant Amazon was not an “Internet company,” he insisted Amazon was the best and cheapest place to buy books.

“Bezos concluded that a true everything store would be impractical — at least at the beginning. He made a list of twenty possible product categories, including computer software, office supplies, apparel, and music. The category that eventually jumped out at him as the best option was books. They were pure commodities; a copy of a book in one store was identical to the same book carried in another, so buyers always knew what they were getting.” — Brad Stone, The Everything Store

The thing that mattered, as it always should, was being the best and cheapest place to buy books. Everything else in the company’s arc followed from that.

We see similar trajectories for Advantaged Commodity companies. They start in some initial market, and then branch outwards into new, related domains. Scale begets power, insights, and new opportunities, and public companies’ market caps indicate the size of the prize.

We’re already partnered with many founders doing this. Our companies are making + processing everything from fish (Shinkei Systems), chemicals (Solugen), wood (TLM), energy (Radiant), precious metals (Earth AI), water (Vital Lyfe), cotton (Stealth), and even more that will be announced soon.

Commodities unlocked an expansive wave of globalization at the turn of last century. They remain rooted in the past, and we’re partnering with founders building commodities for the present — and future.

“If the world economy gets better, commodities are very good place to be in. Even if the world economy does not improve, commodities are still a fabulous place to be.” — Jim Rogers

“Commodities have an intrinsic value, which is not arbitrary, but is dependent on their scarcity, the quantity of labour bestowed in procuring them, and the value of the capital employed in the mines which produce them.” — David Ricardo

If you’re building in commodities, let us know.

Grant is a Partner at Cantos, where he invests in full stack startups, and commodities.